Author: Wang Li Ji, senior expert of IT distribution industry

You use cell phones and digital gadgets every day, but do you know how they get from the manufacturer to you? In fact, before hypermarkets and e-commerce, there is another important link, namely IT distributors. IT distributors link manufacturers and stores and act as an important bridge of logistics, information flow and capital flow in the process of IT products from production to consumption.

The production of IT products is located in the industrial chain. The significance of the existence of IT distributors is to effectively eliminate the information asymmetry between product manufacturers, tens of thousands or even hundreds of thousands of retail terminals and a larger number of consumers, improve the efficiency of the flow of IT products from product manufacturers to final consumers, and realize the socialized professional division of labor. With IT distributors, IT product manufacturers can focus on product production and research and development, and IT retail terminals can focus on product sales and do what they are best at, thus greatly improving efficiency.

In fact, one of the most unknown secrets of IT distributors is that by virtue of their strong financial strength and ability to match funds, they can borrow money for retailers. On the one hand, they can reduce the pressure of downstream funds, and on the other hand, they can generate stable quasi-fixed income returns for themselves.

From the international perspective, the world's main IT distribution listed companies include Ingram Micro, CDW, etc., and domestic Digital China and other related listed companies. Entering September, the semi-annual report of the above companies in 2016 has been released. The following is to interpret the competitiveness of domestic and foreign IT distribution companies by analyzing the data of the above companies' semi-annual reports in 2016. To enrich the data, we also compare the semi-annual figures of ARW, which distributes electronic components, AXE, which distributes cables, and Iacon, which distributes fast-moving consumer goods.

Note: International company unit is USD 100 million, domestic company unit is RMB 100 million. Digital China just completed the backdoor, and last year can not be compared.

First, let's take a look at the international IT distribution listed company data

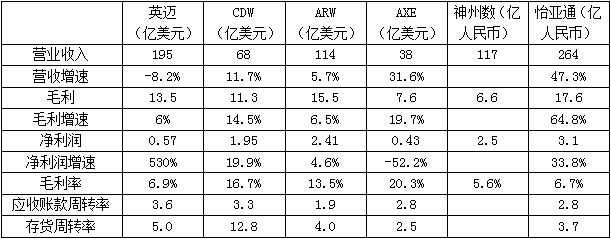

1. Ingram Micro International: The world's No. 1 company with $19.5 billion in revenue

Ingram Micro is the world's largest IT distributor. Founded in 1979 and listed on the New York Stock Exchange in 1996, the company is headquartered in Santa Ana, California, USA, with 27,700 employees and four strategic regions: North America, Europe, Latin America and Asia Pacific (including the Middle East and Africa). It has established branches in 45 countries around the world, and its business covers more than 160 countries on six continents. It provides sales services to more than 1,800 suppliers and solutions and services to more than 200,000 dealers worldwide. The company's market share in North America and Latin America is number one, and its market share in Europe and Asia Pacific is number two.

Ingram Micro held on to the No. 1 spot with $19.5 billion in revenue, according to the 2016 semi-annual report.

Compared to the same period last year, revenue decreased by 8.2%, mainly due to lower sales in North America, Europe and Asia Pacific due to a reassortment of distributed products. Revenue in North America was $8.32 billion, down 8.2% from the same period last year. European sales of $5.44 billion, down 8.2%; Asia Pacific sales revenue of $4.45 billion, down 11.4% from the same period last year; In Latin America, the company achieved growth, with sales revenue of 1.25 billion yuan, up 5.8% year-on-year.

Ingram Micro posted an increase in earnings despite declining revenue. In the first half of 2016, Ingram Micro reported gross profit of $1.35 billion, up 6% from the same period last year, and gross margin of 6.9%, up 0.93 percentage point from the same period last year. In terms of the final net profit, Ingram Micro achieved a net profit of $56.55 million, compared to $8.98 million in the same period last year, a 5.3 times increase in net profit. In the first half of last year, Ingram Micro recognized a one-time pre-tax asset impairment loss of $121 million due to the cancellation of the future deployment of SAP software, which was the main reason for the low net profit base last year.

In the first half of 2016, Ingram Micro accounts receivable turnover ratio was 3.6, that is, accounts receivable turnover in the first half of the year was 3.6 times. Generally speaking, the higher the value, the better, indicating that the company is easy to collect money from downstream customers, and the risk of bad debts is small. The inventory turnover rate of Ingram Micro is 5, that is, the inventory turnover is 5 times in the first half of the year. Generally speaking, the higher the value, the better, indicating that the company has no overstocked inventory and good sales performance.

2.CDW: The inventory turnover data is the best

CDW is an integrated IT solutions provider based in the United States and Canada. CDW's business ranges from standalone hardware and software products to integrated IT solutions such as mobility, security, data center optimization, cloud computing, virtualization, and collaboration. In the half annual report of 2016, the operating revenue was 6.8 billion dollars, up 11.7% year on year; Gross profit of $1.14 billion, an increase of 14.5%, and gross profit margin of 16.7%, an increase of 0.4 percentage points from the same period last year; Net profit was $195 million, up 19.9% from the previous year. CDW's accounts receivable turnover is 3.3 and inventory turnover is 12.8.

3.ARW: The most profitable

ARW is a provider and service provider of electronic component products and services. The company's products, services and solutions for businesses include material planning, design services for new products, programming and assembly services, inventory management, reverse logistics, electronic asset disposal (EAD) and a variety of online supply tools. In the first half year of 2016, the operating revenue was 11.4 billion US dollars, up 5.7% year on year; Gross profit of $1.55 billion, an increase of 6.5%, and gross profit margin of 13.5%, an increase of 0.1 percentage point from the same period last year; Net income was $240 million, up 4.6 percent from a year earlier. ARW's accounts receivable turnover ratio is 1.9 and inventory turnover ratio is 4.

4.AXE: The highest gross margin

AXE is one of the world's largest distributors of wire and cable appliance products. Axe, through its subsidiaries, specializes in selling communications products, wire and cable, electrical and electronic related networking products. In the half annual report of 2016, the operating revenue was 3.8 billion US dollars, with a year-on-year growth of 31.6%; Gross profit of $760 million, an increase of 19.7%, and gross profit margin of 20.3%, down 2 percentage points from the same period last year; Net profit was $43.3 million, down 52.2 percent from the previous year. AXE has an accounts receivable turnover ratio of 4 and inventory turnover ratio of 4.4.

After comparing the semi-annual report data of international distribution companies, let's take a look at the situation of domestic counterparts

1. Digital China: Leading enterprise in the field of IT distribution in China

Digital China, the largest and broadest IT distributor in China, also released its semi-annual report for 2016. Since Digital China only completed its backdoor listing in the second quarter of 2016, the semi-annual report reflects the financial data of Digital China in the second quarter of 2016. In the second quarter, Digital China reported revenue of 11.7 billion yuan, gross profit of 660 million yuan, gross profit margin of 5.6%, and net profit of 250 million yuan, most of which was a one-time gain from the disposal of five subsidiaries during asset restructuring. Net profit after deduction was 55.05 million yuan.

2. Iyatong: Leading distributor of fast-moving consumer goods

Ingram Micro also has similar business types in China. Ingram Micro focuses on IT distribution, while Igram is mainly engaged in the distribution of fast-moving consumer goods. Its supply chain network covers all over China. Yiyatong achieved a revenue of 26.4 billion yuan in the semi-annual report of 2016, with a year-on-year growth of 47.3%; Gross profit was 1.76 billion yuan, up 64.8% year on year, and gross profit margin was 6.7%, down 0.5 percentage points from the same period last year; Net profit was 310 million yuan, up 33.8% year on year. Iyatong's accounts receivable turnover ratio is 2.8 and inventory turnover ratio is 3.7.

Bottom line: Ingram Micro's global dominance will be harder to shake after HNA's acquisition

From the semi-annual report data, the revenue scale of Ingram Micro far exceeds the international and domestic partners, firmly ranked first in the world. The company's accounts receivable turnover and inventory turnover are at a relatively high level in the industry, which reflects that the company is easy to collect money and has a strong discourse right to downstream customers. Excellent inventory management level, good sales, inventory backlog less.

Compared with the two domestic companies, the income scale of Ingram Micro is far more than them, and the gross profit rate is similar, which reflects the strong management ability of the company. We believe this is one of the main reasons why Ingram Micro's gross margin and net profit are lower compared to CDW, which focuses on the US and Canada region, and ARW, which focuses on the distribution of electronic components, while Ingram Micro covers more than 160 countries and IT full category products worldwide.

The first two are small and refined, while Ingram Micro is large and complete. The former is easy to obtain higher returns when its focus area or category is relatively good, but it also faces certain risks. Because of the different levels of regional economic development and the different profit conditions of different categories in different periods, the short-term profit level of the latter will be lower than the former, but the long-term development potential and sustainability of development will be better.

Ingram Micro's business is so large that it is easy to pursue short-term profit growth by cutting out less profitable categories or regions. Generally speaking, once an asset-heavy industry enters a market, it is difficult to exit easily after investment, because the cost of exit is very high. However, Ingram Micro has an asset-light operation mode, and it is easy to exit some regions or categories, which can release more profits in the short term. Moreover, even if it exits temporarily, it can return when the time or necessity is right. And it's relatively easy to come back because of the experience you already have.

Tianhai is wise to invest in Ingram Micro rather than other international IT distributors. Although the net profit of Ingram Micro is lower than that of other international regional distributors, from a strategic perspective, Ingram Micro's rich resources of upstream suppliers and downstream distributors and mature global supply chain system are of great value.

Chinese mobile phone and electronic commerce enterprises have been seeking to layout overseas market in recent years. In the mobile phone industry, emerging mobile phone brands such as Xiaomi and Meizu have begun to explore selling products in India, Southeast Asia and other markets, while traditional mobile phone manufacturers such as Huawei and TCL have been doing business abroad for many years. In the e-commerce sector, both Alibaba and JD.com have established international business units and are experimenting with countries such as Russia. Ingram Micro is a professional international IT distribution giant, will be a great help for China's IT products to go global, is of great significance to China's IT industry.

The Chinese market has huge potential. Ingram Micro entered China in 1999. Currently, with Shanghai as the operation center, Ingram Micro China has set up branches in more than 25 key cities across the country, 6 distribution centers and 18 secondary warehouses with a total area of over 30,000 square meters and a 100% delivery rate on the same day. The on-time customs clearance rate of imports exceeds 99%, which has a good foundation.

However, in the past, due to the incompatibility with the Chinese soil, the domestic development is far less than Shenzhou Digital, Lianqiang International and other domestic IT distribution leaders. Tianhai Investment belongs to HNA Group, which has developed from a single local aviation enterprise into an enterprise group with aviation, industry, finance, tourism, logistics and ecological technology as the pillars. IT has been deeply cultivated in the domestic market for many years and has rich resources in China. With the support of HNA Group, it is believed that Inmicro will shine on the stage of IT distribution in China.